←Back to Education Center Main

Consolidate Student Loans vs Refinance

This article was originally published for SoFi and is used with permission.

If you’re one of the approximately 45 million Americans who currently have student loan debt, you may have heard the terms “consolidation” or “refinancing” being thrown around. If you’re not sure what these terms mean or how they’re different, you’re in the right place.

Finance is personal and how you choose to repay your student loans is no different. While consolidation might make sense for some borrowers, and refinancing might make sense for others, these options won’t make sense for everyone. Understanding the nuances of consolidation vs. refinancing can help empower you to make financial decisions that work for you.

Part of what makes the difference between consolidation and refinancing difficult to discern is that the two terms are sometimes used interchangeably. There are important differences between them, but they do have some similarities. When boiled down to the most basic concept, consolidation and refinancing both combine or replace existing student loans into a single new loan.

The details of how each work are different, which can naturally cause some confusion. This article aims to provide some clarity for borrowers trying to determine the difference between refinancing and consolidation. Let’s start with a breakdown of the specifics of student loan consolidation.

Option 1: Consolidation

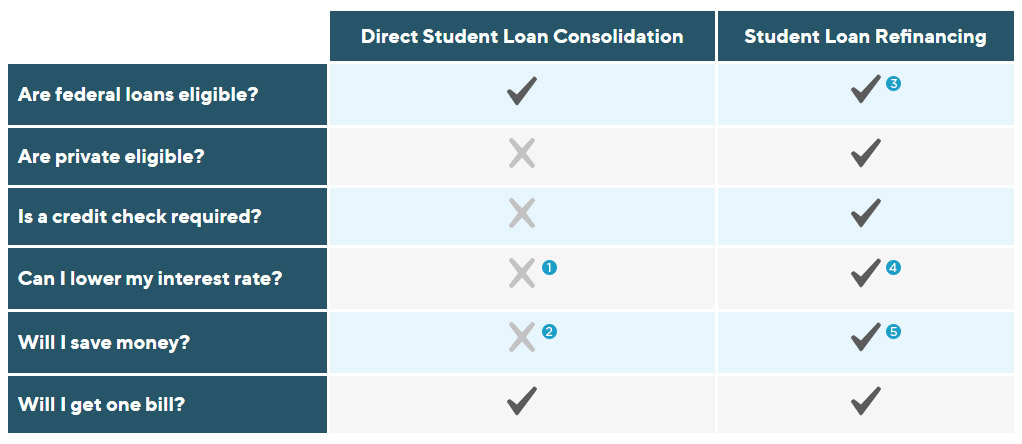

- Direct Consolidation Loan is a loan offered through the U.S. Department of Education that allows you to combine multiple federal education loans into a single federal loan. Only federal student loans can be consolidated through a Direct Consolidation Loan.

- There is no application fee to consolidate loans through a Direct Consolidation Loan.

- The resulting interest rate is a weighted average of prior loan rates, rounded up to the nearest ⅛ of a percent.

- If a borrower’s monthly payment decreases, it’s likely the result of lengthening the term, which can mean paying more interest over time.

- Because the interest rate is a weighted average and not necessarily reduced, federal student loan consolidation is generally not a money-saving option.

-

However, a Direct Consolidation Loan can be a great option for borrowers interested in utilizing federal student loan repayment programs such as income-driven repayment, deferment, or Public Service Loan Forgiveness (PSLF). It’s worth noting that if a borrower has made qualifying payments toward PSLF on existing loans, consolidating those loans could result

in the borrower losing credit for those payments.

Consolidating student loans through a Direct Consolidation Loan might be helpful for borrowers who have a number of federal student loans with different loan servicers. Even though federal student loans are all eligible for the same repayment plans, the government contracts with several different student loan servicers.

This means that even if you hold federal loans exclusively, you could be making payments to more than one servicer. Consolidating your student loans can help streamline your repayment, so you only have to stay on top of a single monthly bill.

Federal loans consolidated through a Direct Consolidation Loan remain federal loans. But instead of having multiple federal loans, you will now have one brand new federal loan with one interest rate, which is the average of your old federal loans combined.

This could be particularly helpful for borrowers who are pursuing federal loan forgiveness or who are enrolled in one of the more flexible federal student loan repayment plans, like one of the income-driven repayment plans

Option 2: Student Loan Refinancing

On the other hand, refinancing is when you consolidate your student loans with a private lender and receive new rates and terms. The exact process can vary by lender, but the general idea is that a borrower consolidates their existing student loan debt with a new loan, and qualifying borrowers might be able to secure a lower interest rate. Here’s some more detail on the refinancing process.

- When a private lender consolidates your student debt, what they are really doing is refinancing your loans.

- Some private lenders will only refinance private student loans. SoFi, however, will consolidate and refinance both federal and private student loans.

- Private lenders review a borrower’s credit score and history, in addition to other financial information, in order to determine the interest rate and terms the borrower qualifies for. Requirements may vary by lender.

- Fees associated with refinancing your student loans are determined by lender. For example, there are no hidden fees when you refinance with SoFi.

- Through refinancing your loans, borrowers receive a new (hopefully lower) interest rate, based on their current financial picture.

- Borrowers with good credit and a strong financial picture could qualify for a lower interest rate and see substantial savings over the life of the loan through refinancing.

- Refinancing federal student loans disqualifies them from federal repayment programs, including PSLF and income-driven repayment plans.

- Borrowers who refinance federal student loans with private lenders will also lose out on federal protections like forbearance and deferment, which give qualifying borrowers the opportunity to temporarily pause payments in the event of financial hardship. Some private lenders have hardship programs in place (like SoFi, which offers unemployment protection for qualifying members), but policies will be determined by individual lenders.

Refinancing can be a solid option for some borrowers, but it won’t be the right choice for everyone. The same can be said for consolidation through a Direct Consolidation Loan. Consolidating student loans via refinancing could be a good idea for people whose financial position—in terms of employment, cash flow, credit, and other factors—has improved since they graduated from school.

Some lenders allow borrowers interested in refinancing to get a quote to see if they pre-qualify for a loan and give them an idea of what rates and terms are available to them. This information could help borrowers determine if they might be able to secure a lower interest rate or more favorable loan terms through refinancing.

People who are working in the public sector or taking advantage of federal debt relief programs such as income-based repayment or PSLF may not want to refinance, as these federal programs do not transfer to private refinance loans.

Looking for more guidance around student debt and financing education? Check out our Student Loan Help Center for education tools, articles, and news around all things student loans.

Understanding the differences between consolidation and refinancing can help borrowers make informed decisions about repaying their student loans. Borrowers interested in refinancing may want to consider SoFi, one of the leaders in the student loan space. You can check your rates in just two minutes.

1 Your interest rate is simply the weighted average of the original loans’ rates.

2 Generally, you won’t see any savings. That’s because your new interest rate is a weighted average of your current loans, rounded up to the nearest eighth of a percent. If you extend your term, you may see your monthly payment decrease, but your total interest payments will increase.

3 Many private lenders only refinance private loans, but SoFi accepts both federal and private loans.

4 Your interest rate will be a new (hopefully lower) rate based on your credit score and other relevant finance data.

5 Reducing interest rate can lower total interest costs and may lower monthly payments, depending on the term you choose.

←Back to Education Center Main